It was a comparatively slow month for Canadian home sales in May as many homebuyers were hesitant to jump into the market before the Bank of Canada cut interest rates. This brought year-over-year national home sales down by 5.9% to 51,219 sales. This spring is one of the slowest in recent years, with Greater Vancouver, Greater Toronto, and Hamilton-Burlington all experiencing year-over-year sales declines of 10% or more.

“The spring housing market usually starts before all the snow has melted, somewhere around the beginning of April, but this year I believe a lot of people were waiting for the Bank of Canada to wave the green flag,” said James Mabey, Chair of CREA. “That first rate cut is expected to bring some pent-up demand back into the market, and those buyers will find there are more homes to choose from right now than at any other point in almost five years. If you’re thinking about jumping into the market now that interest rates are moving down, hire a REALTOR® where you live – or might like to – today.”

Sales Dip in Major Cities But Prairies See Gains

Many of the country’s largest real estate markets experienced month-over-month sales declines in May, which was expected as many buyers were waiting until after the Bank of Canada’s June 5 announcement to make homebuying decisions. Month-over-month sales decreased by 1.4% in Greater Toronto, 2.7% in Montreal, 3.9% in Greater Vancouver, and 5% in Hamilton-Burlington.

Markets in the Praires still made sales gains in May, with Calgary month-over-month sales up by 8.9%, Saskatoon up by 11.3%, and Winnipeg up by 23.1%. As affordability tightened in Ontario and British Columbia, the Prairies have been attracting out-of-province buyers for several months thanks to their relatively lower home prices. But now that the Bank of Canada has announced it is lowering the overnight lending rate, homebuyers in Ontario and British Columbia may return to their markets and increase sales.

New Listings Continue to Soar

Building on the momentum of last month, new listings continued to surge onto the market across the country. Nationally, new listings were up by 8.6% from April and up by 13.5% from last year, an indication that housing inventory is at a much healthier level than previous years.

The largest year-over-year increases in new listings were experienced in Kitchener-Waterloo and Victoria, where new listings rose by 36.1% and 33.7% respectively. Many Ontario cities, including Hamilton-Burlington, Niagara Region, Ottawa, and Greater Toronto, experienced improved housing supply conditions this year, with year-over-year new listings increases of over 15%. From April, the greatest month-over-month increases in new listings were experienced in Thunder Bay and Calgary, with both market’s inventory rising by more than 20%.

Balanced Market Keeping Prices Stable

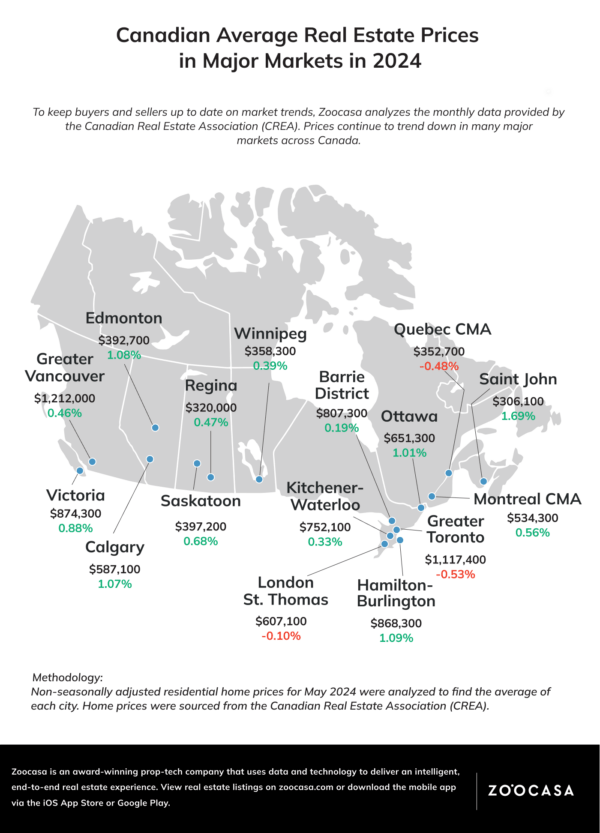

The boost in housing supply, coupled with softening demand, has balanced out the Canadian housing market. This has led to minimal benchmark price gains, or in some cases has flattened home prices. Month-over-month, Saint John led the way with home price gains of 1.69%, followed by Hamilton-Burlington with an increase of 1.09% and Edmonton with an increase of 1.08%.

Quebec, Greater Toronto, and London & St. Thomas experienced month-over-month price declines, with Greater Toronto’s benchmark price decreasing by 0.53% to $1,117,400. May was also the first month this year where the national benchmark price experienced a month-over-month drop, although a very minimal one, decreasing by 0.11% to $733,300. As activity ramps up following the Bank of Canada’s interest rate drop announcement, buyers should take advantage of the still favorable conditions and act quickly to secure their desired properties.

Market conditions vary from region to region however, so if you’re thinking of entering the market, it’s important to speak with a local real estate agent to learn about conditions in your specific area. If you’re ready to talk about your 2024 real estate goals, give us a call today!